Many people are not quite sure how their credit scores affect their mortgage rate. In the simplest terms, the better your credit score, the better chance you have of qualifying for the mortgage loan that is ideal for you. This could mean better interest rates, more loan options, and lower costs.

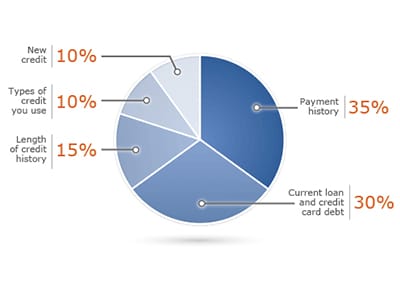

Your credit score is also referred to as your “FICO score”. FICO is an abbreviation for the “Fair Issac Company, the developer of the original scoring model. The credit score that FICO gives you in a number between 300-850, with a higher number being a better score. The score is based on many factors, such as past late payments, debt utilization, and the age of your active accounts. However, how the final score is exactly calculated has not been released, as it is a trade secret closed protected by Fair Issac Co. It is very important that you know and understand your credit score before you start evaluating mortgage loan options.

Two Ways to Get Your Credit Scores:

1. Go to www.myfico.com and sign up to obtain your credit score directly from FICO. Be careful that even though you can obtain your score for free, you must then cancel your free trial within 10 days to avoid being charged for 3 months of service.

2. Use www.creditkarma.com. CreditKarma is a truly free way to obtain, and monitor, your credit score over time. CreditKarma is supported by their advertising partners that advertise credit cards, loan programs, and more so that you can use the website free of charge. Credit Karma also offers you advice on how to improve your credit score by analyzing the different factors that make up you total score (length of credit history, hard credit INQUIRES, late payments, etc.)

You can also get your credit report free, once per year, but with no scores, from the government sponsored website www.AnnualCreditReport.com. Beware of the many sites that advertise ‘free’ credit scores, like FreeCreditScore.com. These sites all charge you for a credit monitoring service in order to get your ‘free’ score.

Also, many of these sites do not use the FICO scoring model used by most lenders. In fact, some web based consumer scoring sites may give you a credit score based on a 500-1000 point rating vs. the standard 300-850 that lenders use. You could think you have an excellent score when, in fact, it is sub par, costing you thousands in increased costs when you go to get a mortgage loan.

It is important to note that while your credit score is a key component, it is not the only factor that a lender considers when approving a mortgage. Be sure to contact The Chaffee Team, before you shop for a new home so you know how to improve your chances of qualifying for the loan that is ideal for you.