You may have seen our recent announcement that conforming and FHA loan limits are increasing for 2024. This is great news because it means that two of the most popular types of mortgages are now or will soon be available for larger loan amounts. Higher limits allow homebuyers and homeowners to use these loans for larger home purchases and refinances, which is important after another year of rising home values. Home sellers also benefit when these higher limits help buyers purchase their homes.

Read on for more information about these loan types and the new limits.

Conforming Loan Limits

Conforming loans are popular because they generally offer lower rates, fees and down payment minimums and more flexible qualification requirements than non-conforming loans.

Here’s how conforming limits are increasing:

| Baseline Loan Limits (most of the U.S.) | ||

| Property # of Units | 2023 Limit | 2024 Limit |

| One | $726,200 | $766,550 |

| Two | $929,850 | $981,500 |

| Three | $1,123,900 | $1,186,350 |

| Four | $1,396,800 | $1,474,400 |

| High-Cost Area* Maximum Loan Limits | ||

| Property # of Units | 2023 Limit | 2024 Limit |

| One | $1,089,300 | $1,149,825 |

| Two | $1,394,775 | $1,472,250 |

| Three | $1,685,850 | $1,779,525 |

| Four | $2,095,200 | $2,211,600 |

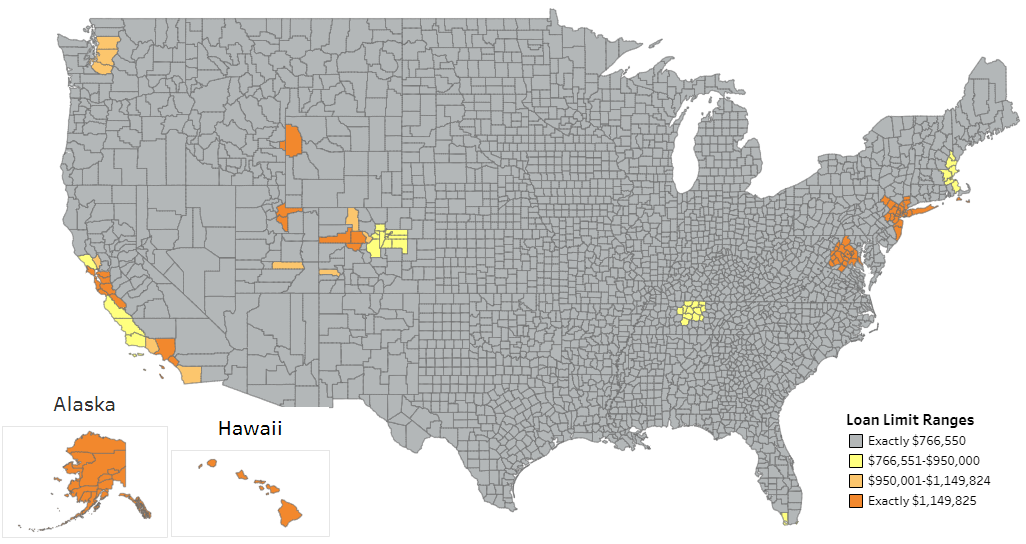

As you can see, most of the U.S. is subject to the general loan limits for conforming loans. However, certain designated “high-cost areas” have higher limits that range between the baseline limits and the high-cost area maximum limits. The map below shows the 2024 limits for 1-unit homes by county across the U.S.

A list and interactive map of the 2024 conforming limits for all counties and county-equivalent areas in the U.S. can be found here.

Draper and Kramer Mortgage Corp. is offering these new conforming limits effective immediately for conforming loans that lock on or after December 1, 2023 and close on or after December 22, 2023.

FHA Loan Limits

FHA (Federal Housing Administration) loans are popular for offering down payment minimums as low as 3.5% and credit score minimums as low as 580.

| Low-Cost Area Floor Loan Limits | ||

| Property # of Units | 2023 Limit | 2024 Limit |

| One | $472,030 | $498,257 |

| Two | $604,400 | $637,950 |

| Three | $730,525 | $771,125 |

| Four | $907,900 | $958,350 |

| High-Cost Area Ceiling Loan Limits | ||

| Property # of Units | 2023 Limit | 2024 Limit |

| One | $1,089,300 | $1,149,825 |

| Two | $1,394,775 | $1,472,250 |

| Three | $1,685,850 | $1,779,525 |

| Four | $2,095,200 | $2,211,600 |

Similar to conforming loans, much of the U.S. is subject to the lower set of FHA loan “floor” limits, while high-cost areas have higher limits that can reach as high as the “ceiling” limits. You can look up the 2024 FHA loan limits for all counties and county-equivalent areas in the U.S. here by selecting a state and the year 2024.

Draper and Kramer Mortgage Corp. is offering the new FHA loan limits for loans with FHA case numbers on or after January 1, 2024.

Conclusion

In summary, thanks to these new increased limits, you may now be able to use a conforming or FHA loan with their flexibilities and benefits for a larger home purchase or refinance than before. If you have any questions about these new limits or would like a free mortgage consultation, please reach out today!

Mortgage programs are subject to approval based on individual program guidelines, borrower’s credit and underwriting approval, acceptable appraisal and clear title. Contact your Draper and Kramer Mortgage Corp. professional for full program details and requirements. Draper and Kramer Mortgage Corp. is a private corporation organized under the laws of the State of Delaware. It has no affiliation with the U.S. Department of Housing and Urban Development, the Federal Housing Administration or any other government agency.